Royal Caribbean Lowers 2026 EPS Forecast as Fuel Costs Rise

Even with ships sailing packed, Royal Caribbean’s softer outlook is a reminder that fuel and geopolitical disruptions are the cruise industry’s biggest swing factors in 2026.

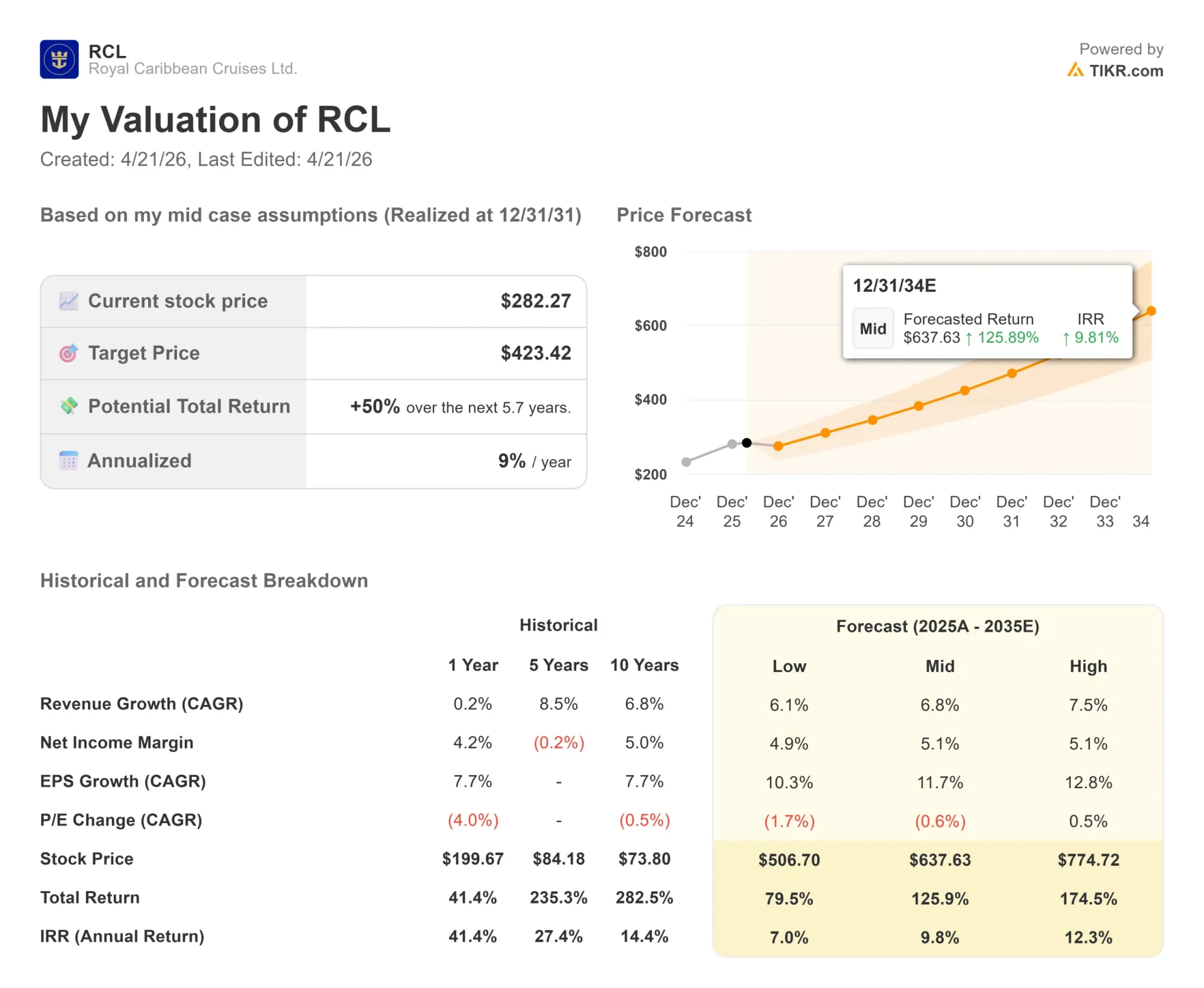

Updated May 24, 2026

Royal Caribbean Group reported first-quarter 2026 results that exceeded its own guidance, supported by higher revenue and cost efficiencies even as the company flagged rising fuel costs and a brief, geopolitics-linked booking slowdown in March and early April.

Quarterly performance outpaced internal targets

Royal Caribbean posted earnings per share of $3.48 and adjusted EPS of $3.60 for the quarter. The adjusted result beat the $3.19 average analyst estimate compiled by LSEG. Total revenue rose 11% year over year to $4.5 billion. The company reported net income of $0.9 billion, adjusted net income of $1.0 billion and adjusted EBITDA of $1.7 billion.

Occupancy and volume stood out. The company reported a 109% load factor, indicating ships sailed above standard double occupancy, and said capacity increased 8% year over year as it served 2.5 million guests, up 12%.

Royal Caribbean said first-quarter net yield growth exceeded guidance because of strong close-in demand and higher onboard revenue. The company cited guest demand for onboard offerings such as specialty dining, Wi-Fi, drink packages and shore excursions, and said 70% of guests are pre-booking extras before sailing.

CEO Jason Liberty said the company remains focused on delivering innovative vacation offerings, pointing to new ships such as Legend of the Seas and destinations including Royal Beach Club Santorini, which is now open.

Demand held up after a brief spring slowdown

After a record WAVE season, Royal Caribbean said demand across its portfolio remained strong, although it saw short-lived booking moderation tied to external events. Bookings for Mediterranean sailings and West Coast of Mexico itineraries softened in March and early April as geopolitical developments, higher air travel costs and flight disruptions weighed on consumers. The company said demand recovered and is now running ahead of the same period last year for remaining inventory.

Close-in reservations stayed strong, contributing to better-than-expected net yield performance during the quarter. By the end of April, Royal Caribbean said its booked position was similar to 2025 at higher prices, with April bookings exceeding last year. CFO Naftali Holtz said that even with global uncertainty, demand for travel experiences has remained solid, adding that consumers are becoming more selective and focused on value in their spending.

Fuel and operating costs moved in different directions

Royal Caribbean reported gross margin yields up 6.9% on an as-reported basis in the first quarter. Net yields rose 3.6% as reported, or 2.0% in constant currency.

On costs, gross cruise costs per available passenger cruise day fell 1.0% as reported. Net cruise costs excluding fuel were up 0.6% as reported and down 0.5% in constant currency.

Fuel was a bigger headwind. Royal Caribbean said first-quarter fuel pricing averaged $613 per metric ton after hedging, with consumption of 432,000 metric tons. For the full year, it expects fuel expense of about $1.3 billion based on current prices, net of hedging, and said the fuel outlook adds roughly $0.62 per share versus prior expectations. The company said it is 59% hedged for 2026 at below-market rates. For 2027, it is hedged for nearly 50% of fuel consumption at an average cost of $408 per metric ton.

Guidance points to midyear pressure before improvement later in 2026

On the earnings call, Liberty described a “smiley face” yield shape for 2026, with more pressure expected in the second and third quarters before improvement later in the year. Royal Caribbean revised its full-year net yield guidance to a range of 1.5% to 2.5%, compared with its earlier range of 1.5% to 3.5%.

The company updated full-year 2026 adjusted EPS guidance to $17.10 to $17.50, compared with its prior forecast of $17.70 to $18.10. The reduction reflects higher fuel costs, the earnings impact of recent geopolitical events, lower net yields and a $0.12 headwind from a lower anticipated contribution from TUI Cruises, partially offset by lower non-fuel costs and the benefit of share repurchases. At the midpoint, the new range still implies about 11% adjusted EPS growth, according to William Blair analyst Sharon Zackfia.

For the second quarter, the company guided to adjusted EPS of $3.83 to $3.93. It expects net yields to rise about 0.9% as reported (0.2% in constant currency) versus the same quarter last year, while net cruise costs excluding fuel per available passenger cruise day are expected to rise 4.9% to 5.4% as reported, driven in part by increased drydock days and higher crew movement costs.

Shareholder returns, liquidity, and refinancing activity

Royal Caribbean returned about $1.1 billion to shareholders in the first quarter, including $836 million in share repurchases and $270 million in dividends. The company repurchased 2.9 million shares for $836 million and said it had $1.0 billion remaining under its current share repurchase authorization at quarter end.

The company ended the quarter with $6.9 billion in liquidity, including cash and capacity under its revolving credit facility. In February 2026, Royal Caribbean issued $2.5 billion in senior unsecured notes maturing in 2033 and 2038, which it said was aimed at refinancing debt and reducing near-term maturities. Net debt remains above $20 billion.

Fleet and destination investments remain central to growth plans

Royal Caribbean said it expects 2026 capital expenditures of about $5 billion, primarily for new ship deliveries and destination development. The company plans to take delivery of Legend of the Seas in the second quarter, with the ship expected to launch this summer. Pricing for Legend of the Seas is running ahead of Icon of the Seas and Star of the Seas at comparable points in their booking cycles.

The company also has Icon VI and Icon VII on order, while continuing destination work that includes Perfect Day Mexico in Mahahual in 2027 and Royal Beach Club Cozumel in 2028.

Royal Caribbean is also expanding into river cruising through Celebrity, with plans to add 20 river ships from 2027 through 2031. The company expects capacity to grow 6.7% in 2026, with annual capacity growth in the 5% range through 2029.

Liberty said the company remains focused on delivering “responsible, differentiated vacations,” while working to accelerate revenue growth and manage costs. Royal Caribbean has said its 2027 Perfecta goals remain in reach, including a 20% compound annual growth rate in adjusted EPS compared with 2024 and return on invested capital in the high teens.

Peer updates at Norwegian and Carnival

Norwegian Cruise Line Holdings reported first-quarter revenue of $2.3 billion and occupancy of 103.8%. Its shares fell about 8% after its first-quarter call, even though earnings per share came in higher than anticipated, as the company did not meet broader Wall Street expectations. Management cited staffing, operating cost and Caribbean capacity challenges, along with pressure from geopolitical developments, including elevated cancellations in Europe.

Norwegian Luna debuted earlier in 2026 and is set to debut in New York in 2027, while the company is expanding Great Stirrup Cay with the Great Tides Water Park scheduled to open this summer. Carnival Cruise Line, meanwhile, reinstated its dividend at $0.15 per share after achieving investment-grade metrics. Its adjusted net income rose more than 60% in 2025, though it continues to face fuel sensitivity and carries a $26.6 billion debt balance.